Snap will begin publicly trading tomorrow, which means that it will officially give a price for its shares in its initial public offering this evening.

Originally setting a range between $14 and $16, the company set its own valuation lower than what tech observers might have expected, given the hype of the first big tech IPO of 2017. But, like all instances of these kinds of IPOs, that’s expected to go up and we’ll likely see where the company wants to set its own real valuation that’s somewhere between giving Wall Street to align the hype and the potential of its business.

More than anything else, though, it’s going to give us some insight into how people are feeling about the company given the major questions that it’s faced throughout its roadshow — a whirlwind trip where it pitches to bankers and retail investors as to why they should buy the stock. It’s spent the past few weeks in ballrooms and hotels fielding questions and we’ll see if they were actually able to quell concerns, or if that was going to affect any demand in the first place.

Here are a couple of key questions that the company faced during its pitches, and where we can finally get some insight into how Wall Street and other retail investors are feeling:

What’s the appetite for tech IPOs?

Earlier this year, AppDynamics — a large enterprise company — was expected to go public and give us a sense of what the environment was going to be for tech IPOs in 2017. You’ll hear the phrase as to whether the “IPO window is open,” meaning that for the moment there’s appetite to buy into newly-minted public companies. It’s generally the first IPO of the year that sets the stage.

That data point evaporated when Cisco snapped up the company just days before it debuted publicly, basically taking away an opportunity to gaze into the crystal ball and see whether or not people would be feeling good about buying into these companies. So now Snap is next on the list to demonstrate whether there’s demand from people to buy into newer companies and start placing their bets for the long term.

Snap is still a consumer tech company. So it in some ways isn’t particularly helpful when setting up comparison models for enterprise companies that are more frequently the ones going public. A big and hyped IPO like Snap doesn’t come around that often, but based on how oversubscribed the deal is and what the day one “pop” is will gauge what kind of confidence investors have in tech companies going public this year.

Will Wall Street forgive Snap’s huge costs of revenue?

Snap has signed huge contracts with Google and Amazon for their hosting services, where Snap runs its operations. These contracts were not cheap — they’re in the billions of dollars — and already Snap’s costs of revenue are huge. Its revenue is growing at an amazing rate, but the rate at which it’s burning cash is almost equally as remarkable. It’s going to be a problem as Wall Street is looking for (and rewards) a company that can be a sustainable and profitable company that can continue to grow.

This is going to be a long-term situation for Snap as it continues to work with hosting providers, rather than take the approach of other video streaming companies with their own infrastructure and hardware. It doesn’t just mean that Snap going to have to rely on the stability of those services — it means its costs are going to continue to scale with its users.

There are alternative ways to drive this cost down. On a purely speculative level, it wouldn’t be surprising if Snap were working on new kinds of tech to get the compute costs of getting its videos and Snaps from one person to another, especially as it broadens its portfolio of camera and video products. Instagram has the luxury, with stories, of piggybacking on huge infrastructure, but Snap has to figure out a way to get this under control.

Still, this may be moot. Given that a huge bet is being placed on Snap CEO Evan Spiegel, it may be that investors are going to place their faith that its revenue will eventually outpace its costs, or that it’ll figure out a way to get that under control.

Is Evan Spiegel’s control of the company — and the structure of the IPO — a real concern?

Snap’s IPO is unprecedented in a lot of ways, but there’s one that stands out: Snap is not selling stock with voting rights. That means that when investors buy shares, it’s going to basically be on the hope that it’ll be a growth company. They won’t be able to have any impact on the decisions that Spiegel and others make, so they are basically buying a long-game, wait-and-see stock to see if the bet plays out.

So for Wall Street, a lot is going to be riding on Spiegel. One thing that the pricing (and day-one stock move) will indicate is whether Spiegel and other executives like COO Imran Khan were able to impress bankers and investors enough during the road show. Spiegel and company, it seems, were able to maneuver around the key questions that investors may have had and still pack the rooms of the hotels he visited as part of the roadshow.

Betting on the founders and top team is always part of the question. A big part of Twitter’s IPO would be whether then-CEO Dick Costolo would be able to maneuver the company into a massively successful and sustainable one. So if it’s successful, it may be that investors seem to have enough confidence that Spiegel can pave the way to a successful future for the company.

Did Snap quell concerns about user growth?

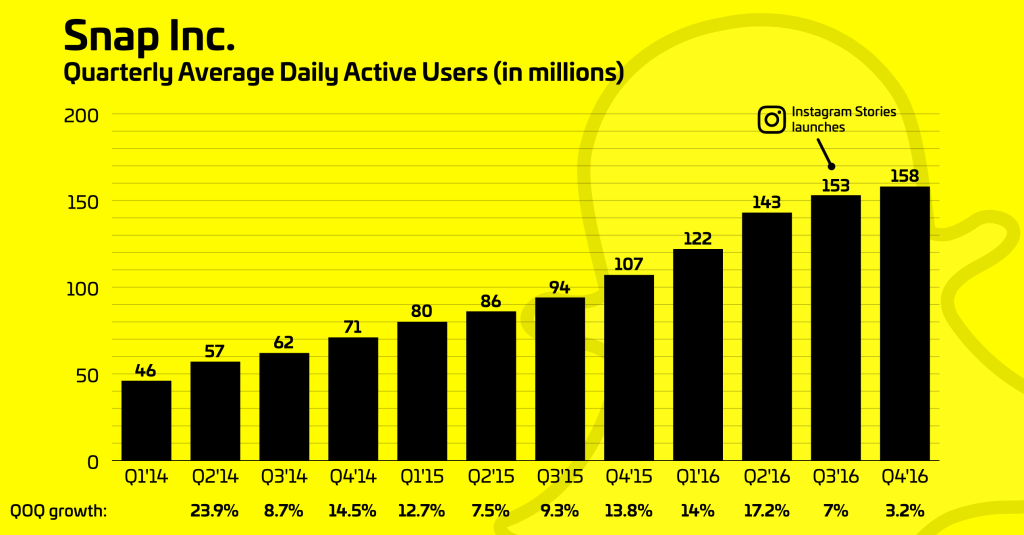

One of the biggest questions about Snap’s IPO was whether or not its slowing user growth would be a major issue for the company going forward. A big advertising business like Snap’s can grow in multiple ways (including better targeting and new products), but at the end of the day still scales with user growth and user engagement.

Spiegel and company pointed to issues with its Android app, which may have impacted user growth, during the roadshow. And Snap is still dueling Instagram and Facebook copying its products like Stories, which could siphon away Snap’s users. It’s going to have to start expanding internationally, but it looks like it’s having a lot of issues there. The concern with Snap is that Wall Street will have another Twitter on its hands — which couldn’t grow its user base and wasn’t able to do a better job of monetizing them.

All this being said, Snap is still a young company, and that it’s been able to attract more than 150 million daily active users and has only recently begun monetizing them may have been a strong enough signal for Wall Street. Spiegel and Snap may have been able to answer the questions in the right way, such as with new products and improving their apps, to quell those concerns. And alternatively, it may have made a good enough pitch that its engagement is high enough that it can still do a better job of monetizing its users.

Snap’s advertising business and other products are still very young — is that still enough to make a big bet on Snap?

Snap is very early in the monetization of its user base. While it’s already begun amassing a large advertising business — and at the very least attracting the innovation budgets of advertisers — it’s only recently started building that business. A lot of comparisons are going to be drawn between ARPU comparisons between Snap and Facebook, but the company still needs to show that it can scale that up.

That being said, it may be that the limited amount of data for its advertising growth won’t be a major concern. Investors already had a good look at Facebook and Twitter’s businesses while going public, but these bets are still on growth. That doesn’t always go in a straight line, as we’ve seen with Facebook, but the outcome can be equally successful if Snap makes the right decisions along the way.

So it could go one of a couple of ways: Snap’s growth and advertising is a sticking point and is going to introduce some pessimism; or its growth is great in its early stages, and that’s enough to go on for now. That’s going to be one of the more risky bets for Snap, and we’ll see if it was able to wield a larger valuation based on projections for its future success.

Featured Image: Michael Nagle/Bloomberg via Getty Images